The biggest mistake women make when it comes to investing, with Kristen Lunman

When it comes to investing, women’s biggest mistake has nothing to do with how they invest.

In fact, studies have shown that women are often better investors than men! Our number one mistake is that we’re not investing enough.

The modern woman is independent, earns good money and has access to all kinds of investment opportunities that our mothers never had.

Yet, many of us stick to playing it safe in savings accounts with rock-bottom interest rates.

When it comes to money matters, we often don’t feel as confident as men, and we can worry ourselves into inaction triggering an anxiety loop of where do I start? How much should I invest? What should I invest in?

It can become so overwhelming that we might think, “investing just isn’t for me”.

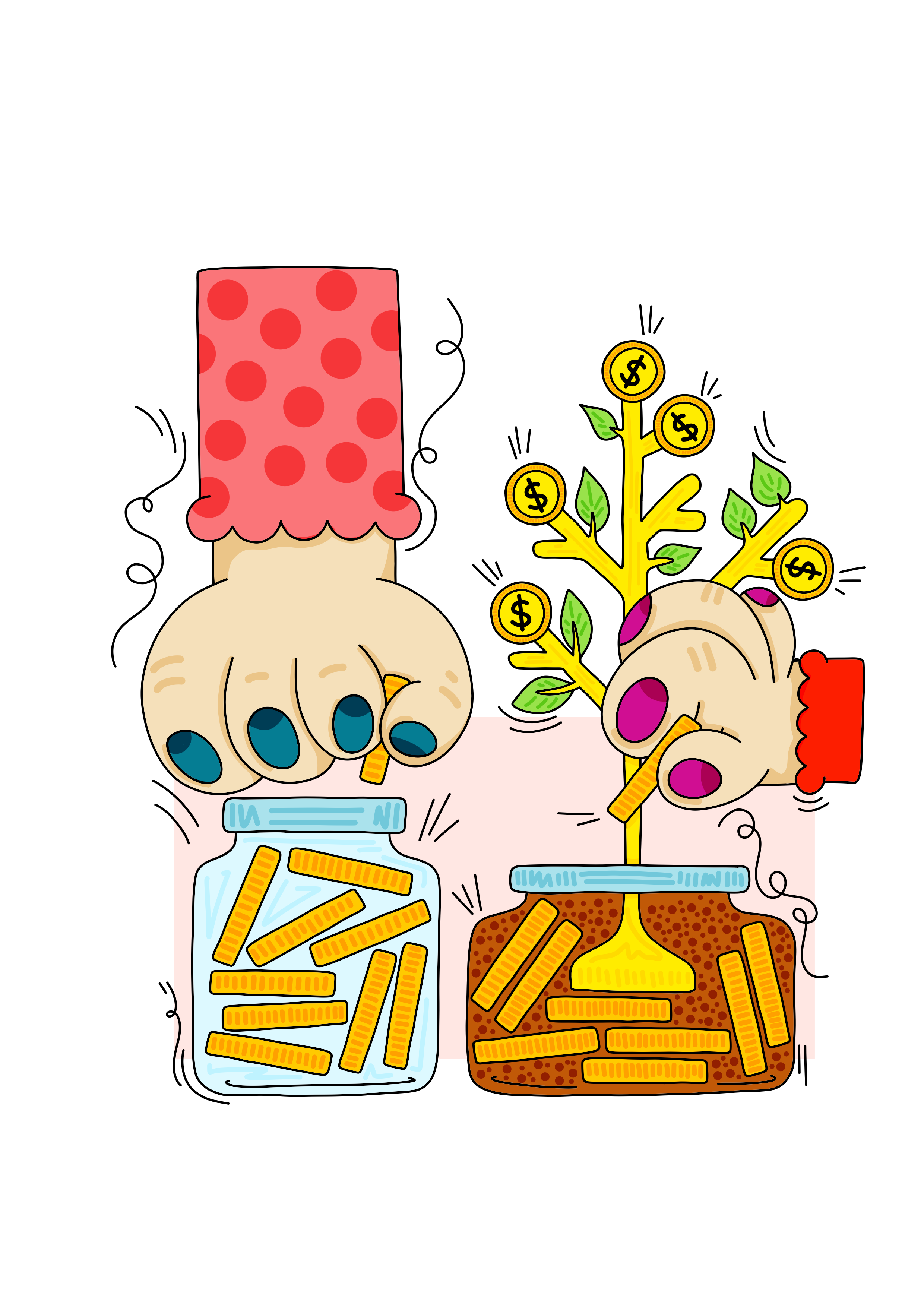

Most women feel like they’re good savers, but there’s a big difference between saving and investing.

Savings are intended to be used as a safety net when life throws us curveballs or short-term goals like that ski trip in Otago.

Investing gives us the ability to take control of our financial future and achieve long term goals like quitting a job for a career change or that retirement bach in Northland.

What about share market risks?

Without some risk, there’s no opportunity for investment return. You can’t reap the rewards of investing without hitting some bumps along the way.

Just keep in mind that even with the occasional share market drop, historically, the US and NZ share markets have provided good returns with a long-term average of around 10% growth per year.

Say you have $10,000 sitting in a savings account, and you plan to set aside another $500 a month with the hopes of growing your money over the next 30 years.

You could put the money in a “high interest” savings account, like a term deposit, or invest it in the share markets.

The best term deposit rates are currently below 2%, and savings accounts only earn around 0.5%.

If you add your $500 monthly contribution to your $10,000, you’ll have about $113,582 after 30 years in a savings account.

But what happens If you invest your $10,000 in the share markets, and every month you invest the additional $500?

If you assume average returns of 10% per year over 30 years, you could have around $665,571 instead. But you don’t have to start with $10,000.

Instead, think about starting with something like $100 and look at it as an investment in your financial education.

Choose a company that you know well or research a popular exchange traded fund (ETF) that spreads your money across hundreds of companies in one go.

You can make automatic monthly deposits to build up your investment portfolio over time.

You’re not too busy, it’s not too complicated, and it just might be something you’re good at!

Investing has changed thanks to modern investing platforms that use technology to make it more affordable and accessible.

If you’re currently doing things like booking flights online or use online banking, you’ll probably be surprised with how easy buying shares can be.

All you need to do is open an online account, transfer money into it, and place an order.

And voila: you’re a shareholder in the causes you believe in and the brands you use every day. It’s never too late to start.

You work hard for your money, so now could be the perfect time to make sure your money is working hard for you.